A Century of American Real Estate

Cycles, Wealth, and the Investment Horizon

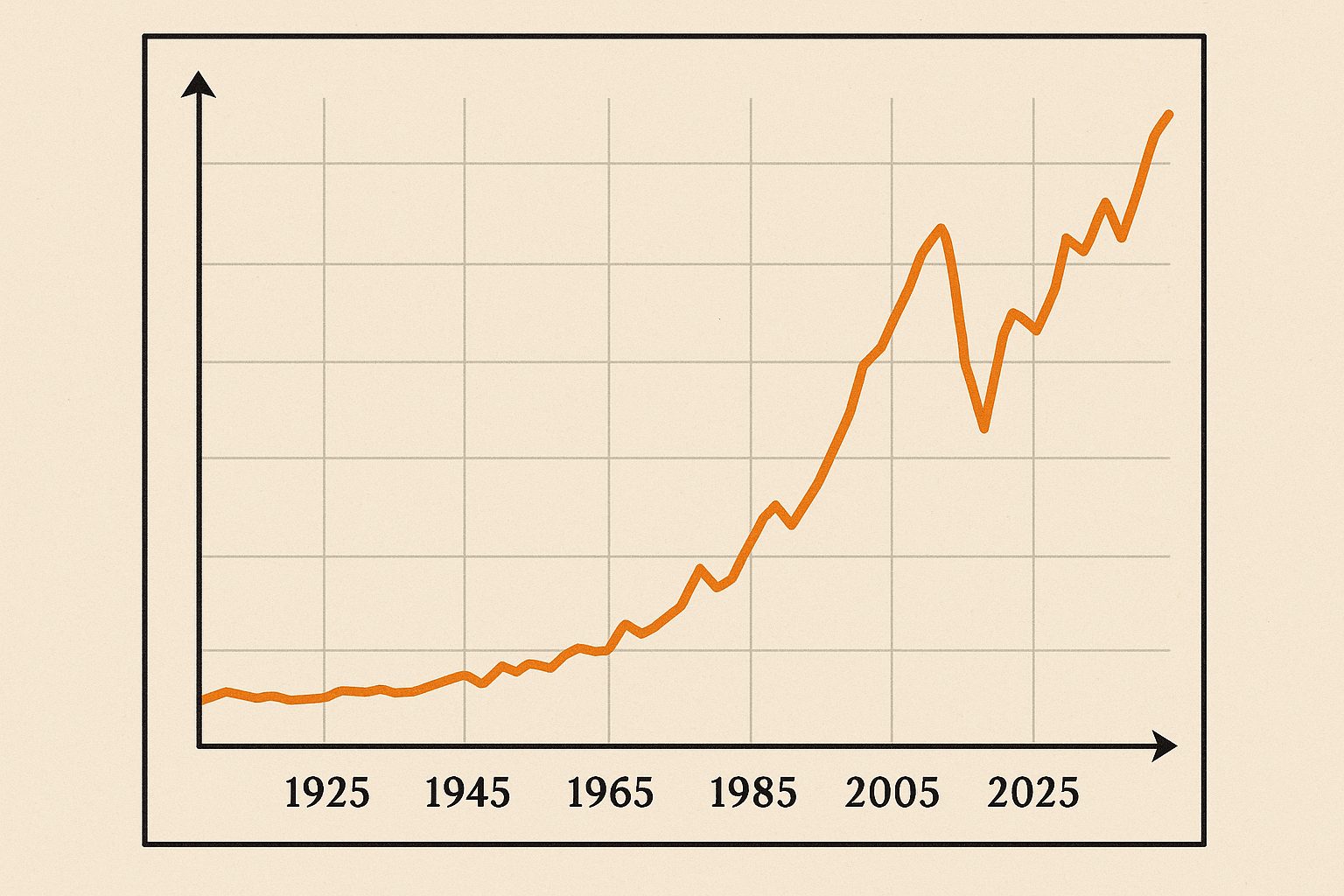

Part I: The Great American Real Estate Cycle: A 100-Year Retrospective (1925-2025)

The history of the U.S. real estate market over the past century is not a story of linear growth but one of dramatic, often violent, cycles. These cycles of boom and bust, expansion and contraction, are driven by a complex interplay of economic fundamentals, demographic shifts, technological innovation, and, most critically, the guiding and sometimes heavy hand of government policy. Understanding these historical patterns is not merely an academic exercise; it is essential for any serious investor seeking to navigate the complexities of today’s market and anticipate the currents of tomorrow. From the forgotten bubble of the 1920s to the post-pandemic “Great Freeze,” each era offers distinct lessons on the creation and destruction of real estate wealth. The following analysis dissects these pivotal periods, revealing the recurring themes that define the American real estate landscape.

Table 1: Key Eras in U.S. Real Estate History (1925-2025)

| Era | Name | Key Market Drivers | Dominant Government Policies | Homeownership Rate Trend | Median Home Price Trend (Nominal) |

|---|---|---|---|---|---|

| 1925–1940 | The Forgotten Boom & Depression’s Reset | Nationwide construction boom (mid-1920s), easy credit, speculation, followed by credit collapse, mass foreclosures, and economic depression.[1, 2] | Creation of Federal Home Loan Bank System (1932), HOLC (1933), FHA (1934), and Fannie Mae (1938) to stabilize finance and create the modern mortgage.[3, 4, 5] | ↓ to 44% | ↓↓ |

| 1940–1970 | The Post-War Suburban Boom | Pent-up demand, Baby Boom, rising incomes, mass-production building techniques (e.g., Levittown).[3, 6] | G.I. Bill (1944) providing VA loans, FHA mortgage insurance expansion, Interstate Highway System construction.[3, 7, 8] | ↑ to 65% | ↑↑ |

| 1970–1990 | The Volatility Decades | Stagflation (high inflation, slow growth), Baby Boomers entering market, energy crisis, manufacturing decline.[9, 10] | Aggressive Fed rate hikes to combat inflation (mortgage rates >16%), S&L deregulation and subsequent crisis, Tax Reform Act of 1986.[9, 11] | ↔ (slight dip) | ↑↑ (volatile) |

| 1990–2010 | The Bubble Economy & Great Financial Crisis | Low interest rates, lax lending standards (subprime, Alt-A), speculative fever, securitization of risky mortgages.[12, 13] | Financial deregulation, government push for homeownership, followed by TARP, QE, and massive stimulus after the 2008 crash.[12, 13] | ↑ to 69% then ↓ | ↑↑↑ then ↓↓↓ |

| 2010–2025 | Recovery, Pandemic Surge & The Great Freeze | Historically low interest rates, QE, rise of remote work, pandemic-fueled flight to suburbs, persistent supply shortages.[7, 14, 15] | Continued low rates, then sharp Fed rate hikes to fight inflation, COVID-related forbearance programs. Focus on local zoning reform begins.[14, 16, 17] | ↓ then ↑ | ↑↑↑ then ↔ (frozen) |

Historical Timeline

Nationwide construction boom followed by credit collapse during the Great Depression. Homeownership rate drops to 44%.

G.I. Bill and FHA fuel massive suburban expansion. Homeownership surges to 65%.

Stagflation and high interest rates (16%+ mortgages) create turbulent market conditions.

Subprime mortgage bubble inflates and bursts, triggering the Great Recession.

QE fuels recovery, then pandemic creates housing frenzy followed by “Great Freeze” from rate hikes.

Key Takeaways: Part I

- Real estate markets move in long cycles (15-30 years) driven by credit availability, demographics, and policy

- Government intervention has been the single most powerful market shaper since the 1930s

- The post-WWII era created the modern housing finance system we know today

- Recent market dynamics (pandemic surge, rate hikes) echo historical patterns

1.1 The Roaring Twenties Boom and the Great Depression’s Reset (1925-1940)

The narrative of American real estate cycles often begins with the post-WWII boom, but a critical, and often forgotten, precedent was set in the 1920s. The decade was marked by a nationwide real estate and construction bubble that, in many ways, was a blueprint for the boom-and-bust cycle that would culminate in the 2008 financial crisis.[1, 2] Fueled by rising incomes, improved credit availability, and a wave of speculative fervor, this boom saw dramatic increases in house prices and construction activity across the country.[10] While the Florida land bubble, where Miami city lots were reportedly traded multiple times a day, is the most famous example, it was merely the most extreme manifestation of a national phenomenon.[2]

This bubble began to deflate around 1926, well before the 1929 stock market crash that officially heralded the Great Depression.[2] The decline in housing prices and construction led to a steady rise in mortgage foreclosures, which were initially viewed as a problem for family farms but soon became a crisis for residential homeowners as well.[2] Research demonstrates a direct correlation between the scale of the 1920s boom and the severity of the subsequent bust; cities that experienced the largest construction booms and price increases in the mid-1920s also suffered the highest rates of mortgage foreclosure in the early 1930s.[1]

Historical Parallel: The 1920s housing bubble bears striking similarities to the 2000s bubble – both were fueled by easy credit, speculation, and ended in financial catastrophe.

The ensuing Great Depression was catastrophic for the housing market. With unemployment soaring to 25% by 1933 and a severe credit contraction, the financial system that supported homeownership collapsed.[5] An estimated half of all urban home loans were delinquent, and foreclosures reached an average of 1,000 per day.[5] As a result, the national homeownership rate, which had been slowly rising, plummeted to a century-low of 44%.[10, 18] This crisis served as the crucible in which the modern American housing finance system was forged, prompting unprecedented federal intervention that would reshape the market for the remainder of the century.

1.2 The Post-War Pact: The G.I. Bill, the FHA, and the Forging of Suburbia (1940-1970)

The period following World War II represents the single most transformative era in the history of American housing. A confluence of powerful forces—the return of millions of soldiers, the demographic explosion of the Baby Boom, massive pent-up demand from two decades of depression and war, and a surge in national prosperity—created an unprecedented need for new homes.[6, 10, 18] It was the federal government’s response to this need that fundamentally re-engineered the American dream, shifting it from the city block to the suburban cul-de-sac.

The groundwork had been laid during the New Deal with the creation of the Federal Housing Administration (FHA), but it was the Servicemen’s Readjustment Act of 1944, universally known as the G.I. Bill, that ignited the boom.[3, 7, 19] This landmark legislation provided returning veterans with access to low-interest, VA-guaranteed home loans that often required no down payment at all.[8, 19] Before this, a typical mortgage required a down payment of up to 58%, an insurmountable hurdle for most working-class families.[6] The G.I. Bill, by insuring these mortgages, effectively eliminated this barrier for millions of veterans.[6] One study estimates that the GI Bill’s housing benefits were responsible for about 25% of the increase in homeownership for the affected age cohorts during this period.[20]

Homeownership Rate: 1940 vs. 1960

This revolution in finance was paired with revolutions in production and infrastructure. Construction firms like Levitt and Sons applied assembly-line techniques to mass-produce affordable houses in vast new suburban tracts, famously known as “Levittowns”.[6] These homes were not only cheap—an early Levittown house cost just $7,000—but were also made accessible through the new government-backed financing.[6] Simultaneously, the Federal-Aid Highway Act of 1956 funded the construction of the Interstate Highway System, creating the arteries that connected these new suburban communities to urban job centers.[7]

The results were staggering. The national homeownership rate, which stood at 43.6% in 1940, surged to 61.9% by 1960—the largest 20-percentage-point jump in the nation’s history.[3] The number of homeowners increased by 55% during this period, and new construction skyrocketed.[3] This era cemented the single-family suburban home as the cornerstone of middle-class American life and established a model of government-supported homeownership that persists to this day. Nominal median home prices reflected this demand, rising from just $2,938 in the 1940s to $17,000 by 1970.[10, 21]

Part II: The Architect of Markets: How Government Policy Shaped American Real Estate

The modern American real estate market is not a naturally occurring ecosystem. It is a meticulously engineered construct, shaped at every turn by a century of deliberate, and often transformative, government policies. From the creation of the 30-year mortgage to the legal battles over fair housing and the overwhelming influence of monetary policy, the federal government has acted as the primary architect of how Americans buy, sell, and finance their homes. Understanding this history of intervention is crucial, as it reveals that the market’s rules are not immutable; they are political choices with profound and lasting economic consequences.

Final Key Takeaways

- Credit cycles drive real estate cycles – access to financing is the primary market mover

- Government policy creates the rules – from mortgages to zoning, policy shapes outcomes

- Demographics create demand – follow population flows to find growth markets

- All real estate is local – national trends provide context but local dynamics determine success

- Total returns matter most – appreciation is just one component of real estate returns